February 2017

Conquering Chaos: Eris on TT’s Trade Talk Blog Election Volatility and its Impact on Interest Rates and Swap Futures in 2017

Written by

Eris Exchange

Christopher Rodriguez, Chief Marketing and Relationship Management Officer

Geoffrey Sharp, Managing Director and Head of Sales

Eris is a U.S. futures exchange that offers listed interest rate swap futures.

Some traders were more prepared than others for the results of the U.S. presidential election in November. Higher implied volatility, changes in risk premium and increases in interest rates resulted from Donald Trump’s surprise victory. Equity markets plunged then rallied. All told, the month of November was remarkable for traders.

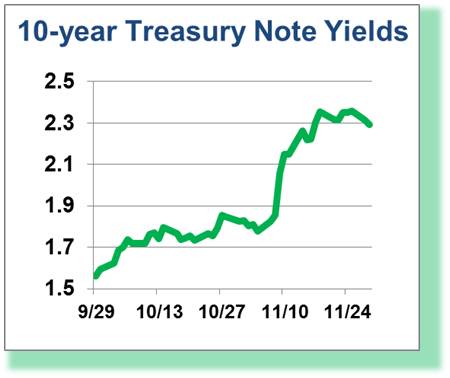

Heading into Thanksgiving, 10-year Treasury Note yields reached highs not seen since mid-2015. The bond sell-off tapered toward month-end, but the forwards predicted a rising rate environment.

Heading into Thanksgiving, 10-year Treasury Note yields reached highs not seen since mid-2015. The bond sell-off tapered toward month-end, but the forwards predicted a rising rate environment.

Some economic outlooks point toward fiscal policy changes that may positively impact economic growth and lead to a continued rise in interest rates. At the same time, some believe the risk remains that global markets underperform and drag on U.S. markets. Specifically, U.S. Treasuries will be appealing to foreign investors causing prices to rise and rates to fall. These competing influences may cause an ebb and flow in rates not seen in almost a decade.

As a direct result of recent shifts in expectations, we’ve seen trading records set across futures markets. CME Group announced an average daily volume (ADV) increase of 52% in November 2016 versus November 2015 and all-time highs in futures open interest of 117mm contracts on November 23rd, of which 69mm contracts were in the interest rate complex (also a record). Eris Exchange recorded an ADV increase of more than 70% in November 2016 versus November 2015, and the low two-day margin Eris Standards more recently set an open interest record of 141,663 contracts on February 3rd.

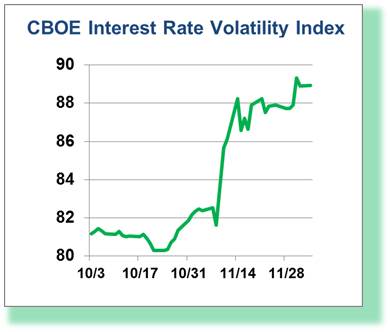

The CBOE Interest Rate Volatility Index illustrates the expected increase in overall rate volatility as it has spiked to recent highs since the election:

The CBOE Interest Rate Volatility Index illustrates the expected increase in overall rate volatility as it has spiked to recent highs since the election:

So what’s next?

Expectations of fiscal easing are already having a major impact on U.S. rates, currently reflected in cash markets, Eurodollars, Treasury futures and swap rates. As the market wrestles with the uncertainty surrounding fiscal stimulus and the possibility of wide-ranging tax cuts by a Trump White House and Republican Congress, expectations of rising inflation and budgetary pressures could lead to continued volatility in the near and intermediate term. Interest rate trading could pick up among both speculators and hedgers, positively impacting both CME Group and Eris Exchange markets.

The combination of competing factors at play, including the uncertainty surrounding decisions that will be made by a Trump administration, will likely result in healthy trading volatility and necessitate increased rate hedging. Indeed, the zero interest rate policy in the wake of the financial crisis has already come to an end and now looks to be reversing course more quickly than expected.

While many market participants cut their teeth trading rates before the financial crisis, others began their professional trading lives after 2008 and only operated in an environment where low rates were the norm. This new generation of traders has the tools and analytics offered through TT and ADL to help them seek out new opportunities to trade rates and accelerate their use and adoption of listed interest rate futures, including swap futures to hedge risks posed by the pending market volatility on the horizon.